New Journal of Physics Volume 16, 2014. Yoash Shapira, Yonatan Berman and Eshel Ben-Jacob.

School of Physics and Astronomy, The Raymond and Beverly Sackler Faculty of Exact Sciences, Tel-Aviv University, Tel-Aviv 69978, Israel..

Abstract

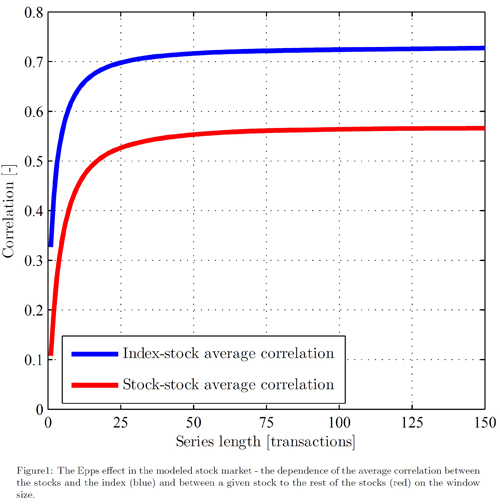

Modelling the behaviour of stock markets has been of major interest in the past century. The market can be treated as a network of many investors reacting in accordance to their group behaviour, as manifested by the index and effected by the flow of external information into the system. Here we devise a model that encapsulates the behaviour of stock markets. The model consists of two terms, demonstrating quantitatively the effect of the individual tendency to follow the group and the effect of the individual reaction to the available information. Using the above factors we were able to explain several key features of the stock market: the high correlations between the individual stocks and the index; the Epps effect; the high fluctuating nature of the market, which is similar to real market behaviour. Furthermore, intricate long term phenomena are also described by this model, such as bursts of synchronized average correlation and the dominance of the index as demonstrated through partial correlation.